Murrey Math Line X untuk MetaTrader adalah indikator yang penting untuk setiap trader yang memahami ...

Indikator Moving Average Candlestick untuk MetaTrader — adalah visualisasi carta yang menunjukkan pu...

Indikator Candlestick Purata Bergerak untuk MetaTrader — adalah visualisasi carta untuk purata berge...

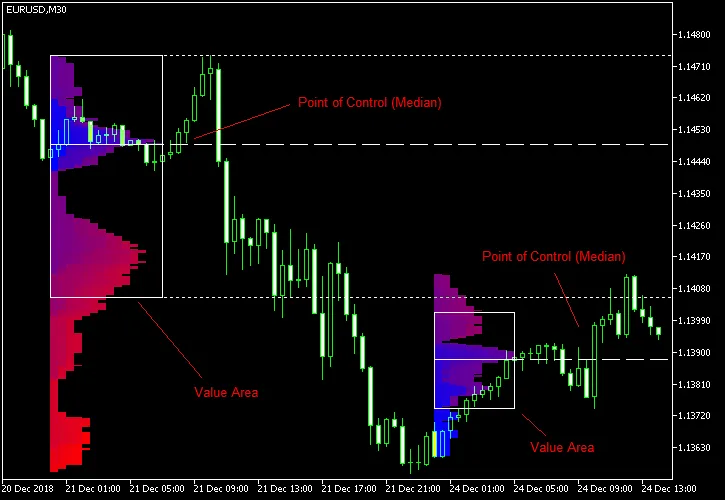

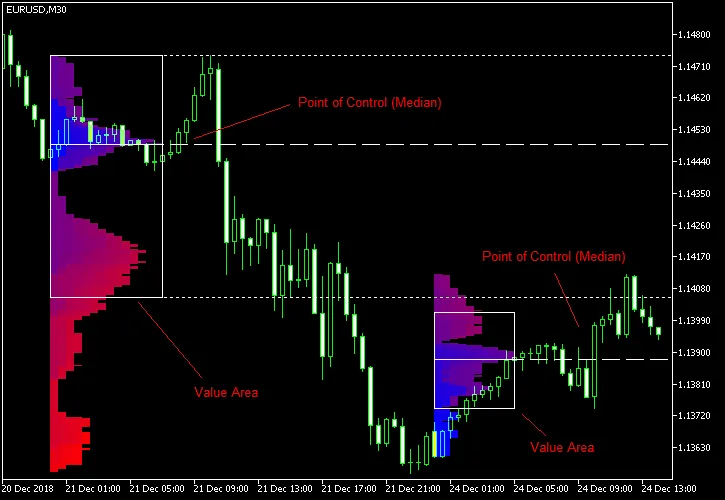

Indikator Market Profile untuk MetaTrader adalah pelaksanaan klasik Market Profile yang dapat menunj...

Indikator Market Profile untuk MetaTrader 4 — adalah pelaksanaan klasik Market Profile yang menunjuk...

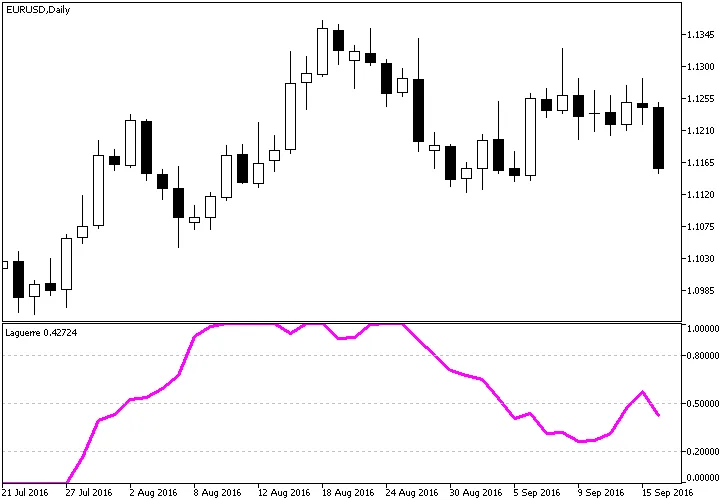

Indikator Laguerre untuk MetaTrader — Ini adalah indikator khusus yang tidak bergantung kepada indik...

Indikator Laguerre untuk MetaTrader adalah indikator yang direka khas dan tidak bergantung kepada in...

Keltner Channel (Indikator MetaTrader) — adalah indikator analisis teknikal klasik yang dibangunkan ...

Keltner Channel (Petunjuk MetaTrader) — adalah salah satu petunjuk analisis teknikal klasik yang dib...

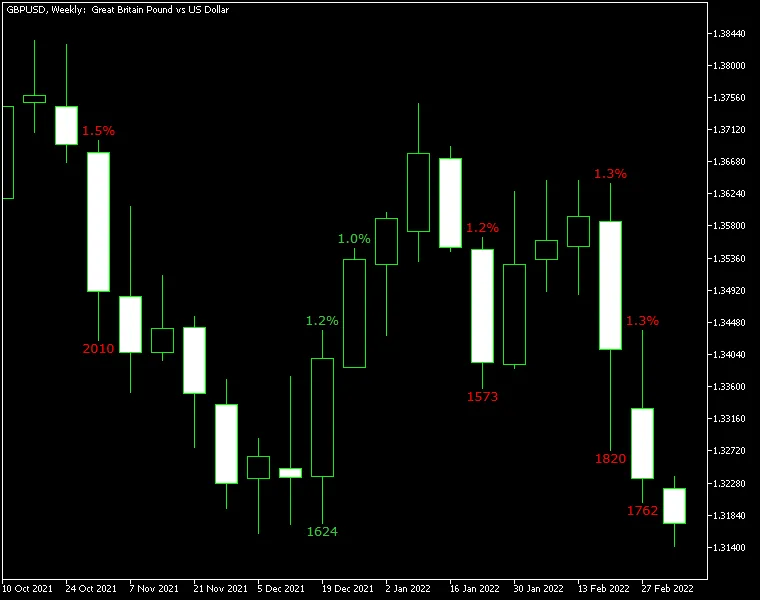

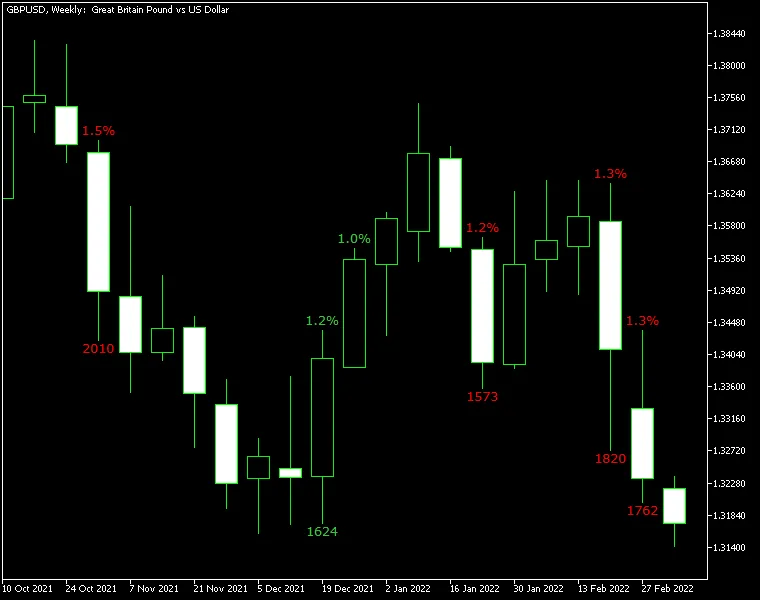

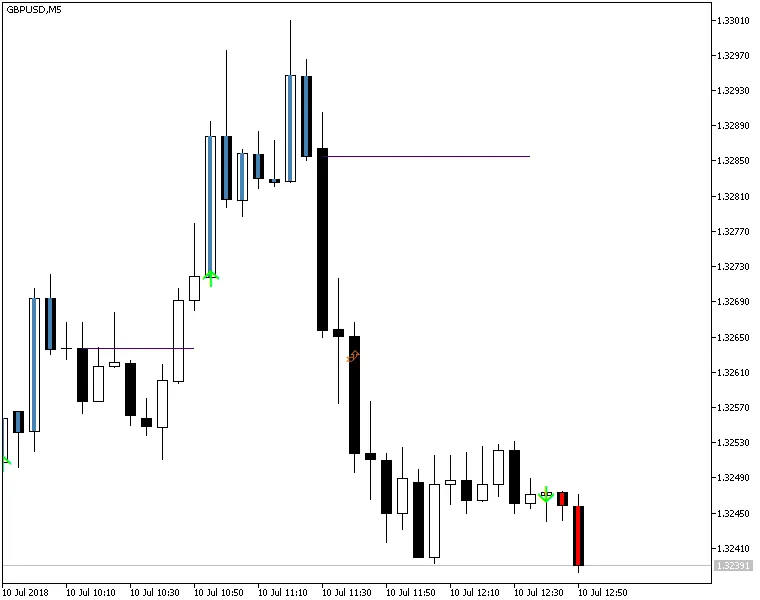

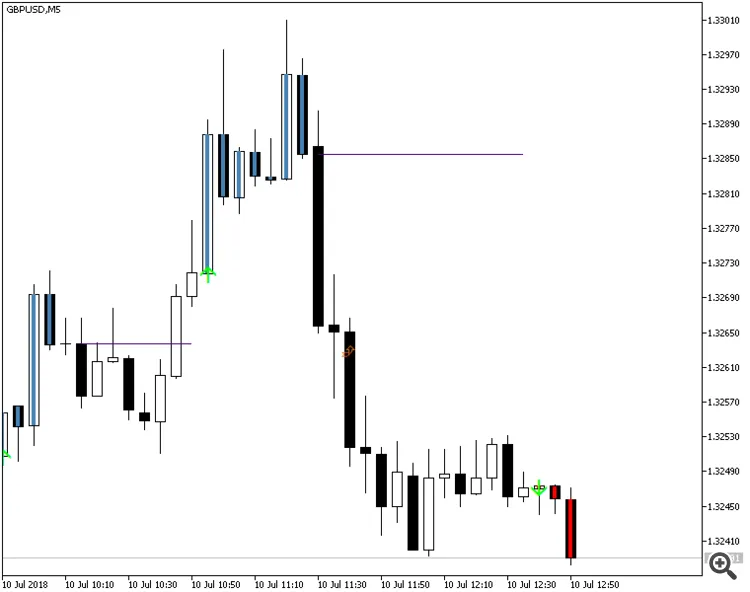

Indikator Maklumat Untung/Rugi untuk MetaTrader — menunjukkan untung dan rugi bagi semua lilin yang ...

Indikator Float MetaTrader adalah alat yang hebat untuk menganalisis sejarah carta bagi pasangan mat...

Indikator Info Untung/Rugi MetaTrader — memaparkan keuntungan dan kerugian bagi semua lilin yang mel...

Indikator Fisher MetaTrader adalah indikator histogram yang cukup mudah digunakan untuk mengesan ara...

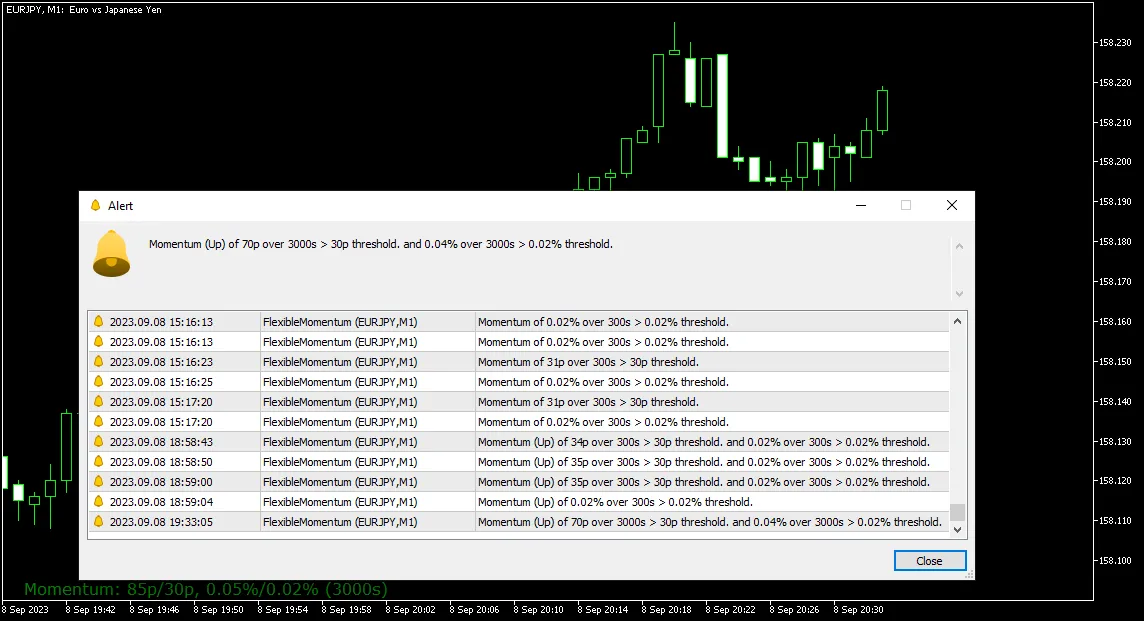

Momentum Fleksibel (Indikator MetaTrader) adalah alat yang mengira perubahan kadar mata wang dalam t...

Indikator Float MetaTrader adalah alat canggih yang membantu kita menganalisis sejarah carta bagi pa...

Visualisasi Trend Mudah adalah indikator MetaTrader yang melakukan apa yang dijanjikannya. Ia menunj...

Indikator Fisher MetaTrader merupakan indikator histogram yang cukup mudah digunakan untuk mengesan ...

Easy Trend Visualizer adalah indikator MetaTrader yang sesuai dengan namanya. Ia memaparkan di mana ...

Indikator Dots untuk MetaTrader 5 merupakan alat yang berguna bagi para trader untuk mengenal pasti ...

Dots Indi (Penunjuk MetaTrader) merupakan penunjuk yang berasaskan indikator dari tahun 2006 oleh Tr...