MetaTrader5

Understanding the Kairi Method (KRI) Indicator for MT5 Traders

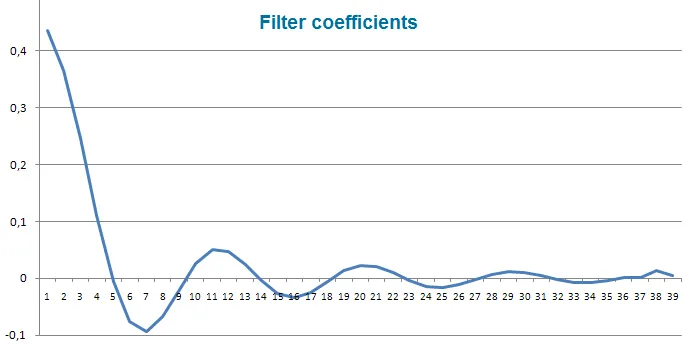

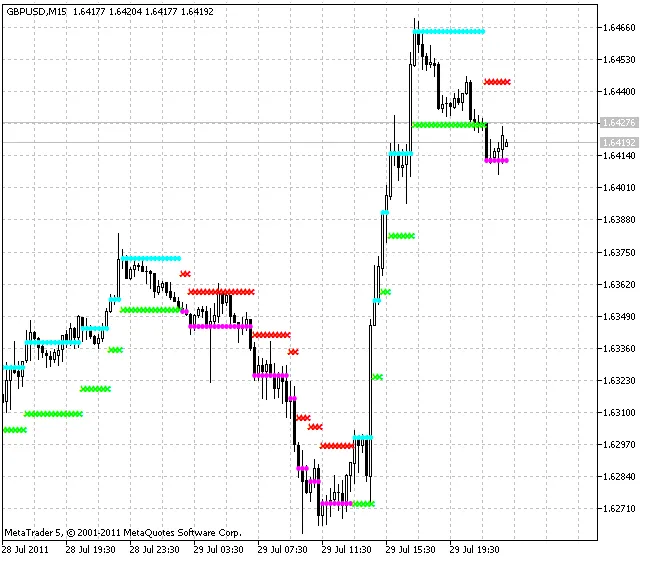

Hey there, fellow traders! Today, we're diving into the Kairi method, commonly known as the KRI indicator. This tool is quite similar to the Momentum indicator in how it operates. The KRI oscillates around the 0 mark, but it has a wider fluctuation range, making it a bit more versatile. For optimal results, a smoothing period of 13 is recommended, and the KRI can be applied across any timeframe. It's one of the simplest oscillators out there! Essentially, it calculates the price deviation from its simple moving average and presents this result as a percentage of that average. Here’s the calculation formula for the indicator: KRI = 100 * (PRICE[bar] - SMA(PRICE[bar], period)) / SMA(PRICE[bar], period) Where: PRICE[bar] - the price; SMA() - the smoothing algorithm; period - the smoothing period for SMA; bar - the bar index. When the price movement lacks a clear trend, a significantly positive KRI value can indicate that the market is overbought, suggesting a good time to consider opening a short position. Conversely, a notably negative KRI value signals a potential buying opportunity. In trending markets, the KRI tends to generate consistent positive values during a downward trend due to the lag between the moving average and the current price. On the flip side, during an upward trend, you’ll see stable negative values. So, if the KRI readings don’t flip from positive to negative (or vice versa) for a while, you might be looking at a trend indicator! Signals pop up when the KRI crosses above +1 (overbought territory) or below -1 (oversold territory) and then retraces back to the center. Pay attention to bullish divergence or bearish convergence between the KRI and price, too, as these can provide additional signals. This indicator utilizes the CMoving_Average class from the SmoothAlgorithms.mqh library for its calculations. If you want to learn more about this class, check out the article on "Averaging Price Series for Intermediate Calculations Without Using Additional Buffers".

2011.09.06